Did you know that your credit score is just half of your financial story? While most of us focus on this one number, your financial health can be improved if you check the details hidden in your credit report. But what exactly is the difference between a credit score and a credit report?

Credit Report Vs Score

Credit reports are a detailed record of your credit history. All financial information, the loans you’ve taken, credit cards you’ve used, payment history, etc., is included in it. The 3 major credit bureaus, Experian, TransUnion, and Equifax, are responsible for compiling this data. Whenever you’re trying to get loans, credit cards, rentals, or even employment, your credit report matters.

Credit score, on the other hand, is a 3-digit number that showcases your creditworthiness. Think of it as a marksheet of sorts, which shows how well you performed financially. It is derived from your credit report using different “scoring models” like the FICO® and VantageScore. Your credit score tells a lender or credit provider how likely you are to miss a payment. The higher your score, the less risky you are as a borrower, hence you qualify for better interest rates and terms.

How Is Credit Score Calculated?

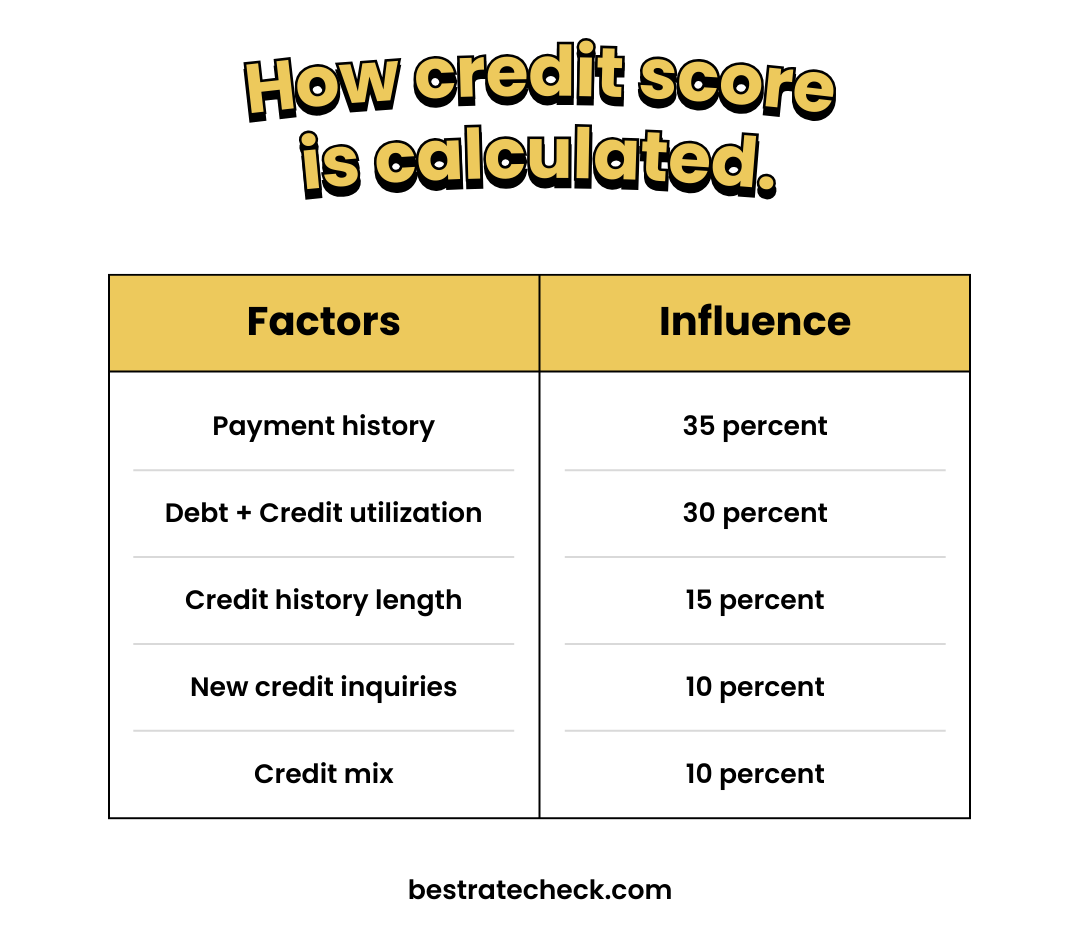

Credit scores are compiled based on your credit report. Everything, from your payment history, amounts owed, length of credit history, new credit inquiries, and credit mix, is taken into account. The first, most important factor that influences your credit score (by 35%) is payment history.

Other important things, like how much you owe, your credit utilization, etc., compare the total debt you have to the credit available. Collectively, these two things make up 30% of your score. The length of your credit history shifts 15% of your score.

And, any new credit inquiries on you, based on the number of accounts you have opened recently, and how long it has been since you opened those new ones, determines 10%. Lastly, credit mix, or the different types of credit accounts you have, changes your score by 10%.

Note that different scoring models may weigh these categories differently. Here’s a summary:

Information Included in Credit Report

Your credit report has your credit history and personal information. Details like your full name and any alternative names you may have used in the past are mentioned. For example, surnames before marriage, nicknames, or your name without the middle name.

Moreover, any credit accounts you have had within the past 7-10 years are also included. The type of account (mortgage, installment, revolving), credit limits, payment history, and account status are all shown. If lenders or credit providers have inquired, that is on your credit report, too.

So, activities like applying for new credit, public records like bankruptcy, foreclosure, tax liens, and judgments are all visible in your credit report. This report is then used by credit reporting agencies (FICO®, Vantage Score) to generate your credit score.

Errors in Your Credit Report

Sometimes, there can be some inconsistencies or errors in your credit report. That may lower your credit score due to faults. You’ll have trouble getting new lines of credit or the terms may get more expensive for you. The Federal Trade Commission (FTC) has noted that one in every five people has an error in at least one of their credit reports. They may be costing you money! It is therefore advised that consumers keep reviewing their credit reports regularly.

How Often Should I Check My Credit Report & Score?

You should keep checking your credit report regularly. You’ll be able to monitor and catch any errors or potential fraud early on, protecting your credit health in the long run. At the maximum, you can keep a one-year gap before you check your report again. But, you might want to check more frequently if you can, especially if you’re building new credit, repairing poor credit, or planning to apply for a major loan anytime soon (like a mortgage or car loan).

As for your credit score, you should check it more often. If you’ve recently challenged something on your credit report, that may be a good reason to track the progress. There is a common myth that if you check your credit score too often, it lowers. But that’s not true.

Can I Check My Credit Score for Free?

You can check your credit report weekly, that too for free and without affecting your score, at AnnualCreditReport.com.

Credit Freeze and How to Do It

The three major credit bureaus let you freeze your credit as a security measure. This can be done online, using your phone, or by mail. Also known as a security freeze, this process restricts anyone, even creditors, from viewing your credit report. However, you can still view it.

By doing this, you can make sure that you’re not a victim of identity theft, and nobody is borrowing credit in your name. The information needed to approve new loans cannot be seen by the credit provider. So, no loan applications are approved. Though it doesn’t mean that you don't need to review your credit report anymore. There are still errors or existing account fraud that may occur.

What Can I Do to Improve My Credit Score?

Making your credit score better is seen as challenging, but it is actually easier than you think. Sure, your financial situation may be tough, but with consistent steps in the right direction and responsible financial behaviour, you can improve your credit score.

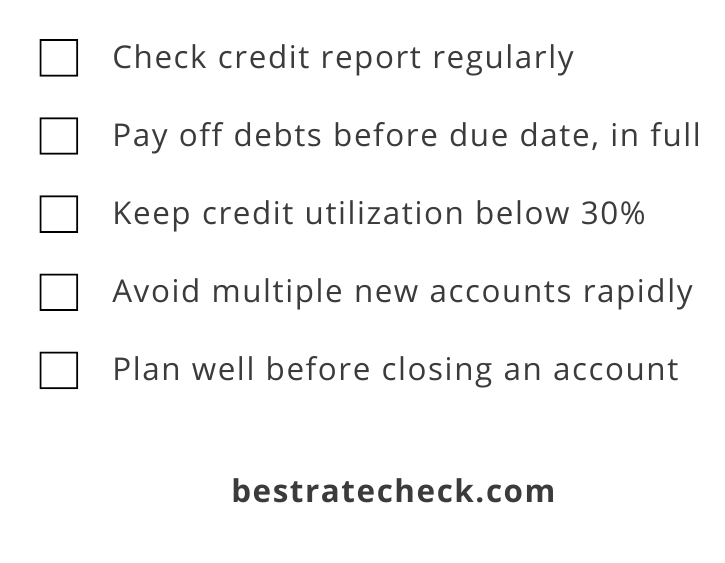

First of all, check your credit report. Look for any errors, inconsistencies, or fraud. If you find anything wrong or suspicious, immediately report it to the credit bureaus and your lender. Also, one of the simplest answers to improving your credit score is to pay off all your debts on time in full. Let’s say you have a credit card balance. Pay it in full every month until the due date. Remember that payment history makes up most of your credit score?

Keep your credit utilization under 30 percent. That is another factor that affects your credit score significantly. If you’ve crossed the limit before, start fresh and follow the rules from now on. If you’re feeling that the credit isn’t enough for you, ask for a limit increase with your credit card company.

Additionally, avoid opening many accounts rapidly. This behaviour signals the credit bureaus that you’re in some sort of financial trouble, specifically if you’re still new to credit with less history. Most importantly, pay off your debt instead of moving it around! If you’re stuck in debt, make a payment plan. Pay off high-interest debts first, and make minimum payments on the others.

Lastly, be cautious about closing your old credit card accounts. Doing so can reduce the average age of your credit accounts and increase your credit utilization ratio, causing a temporary dip in your credit score. See all of this as a game, where every move has a consequence on your score.

Credit Report in the Eyes of Lenders

When you request a loan from banks or online lenders, they don’t know you personally. They don’t know if you’re one of those borrowers who repays. To assess if you’ll be able to pay back, and what the risk of lending to you is, they rely on your credit score. They check your credit report, too.

Your credit score is the complete snapshot of your creditworthiness, and your credit report is your entire financial history. The credit provider will know every little detail. They see your payment history, outstanding debts, credit utilization, etc., before choosing to approve you.

Got a bad credit score? Don’t worry. Lenders don’t look at just this one factor to approve you. They consider your income, current debts, employment status, and sometimes even your educational background to get a broader idea of your profile.

Fico Vs Vantage Score

| FICO | VantageScore | |

| Score Range | Exceptional: 800-850Very Good: 740-799Good: 670-739Fair: 580-669Poor: 300-579 | Superprime: 781-850Prime: 661-780Near prime: 601-660Subprime: 300-600 |

| Calculation Method | Simpler model, uses 6 categories: Payment history, Credit utilization, Credit age, Types of credit, Recent inquiriesUtility payments It rewards full balance payoffs. | Requires 6 months of credit history |

| Credit History Requirements | Simpler model, uses 6 categories: Payment history, Credit utilization, Credit age, Types of credit, Recent inquiries, Utility payments It rewards full balance payoffs. | Requires only 1 month of credit history |

| Industry-Specific Models | FICO Auto Score | None |

| Treatment of Collections | Generally, ignores small collection amounts (original balance below $100) | Excludes paid collections but includes all unpaid collections regardless of amount |

| Credit Utilization Weight | Weighs credit utilization at 30% | Weighs credit utilization at 20% |

| Score Availability | More widely used by lenders, 90% of lending decisions are based on FICO scores | Getting popular slowly |

Borrow & Improve Your Credit Score

If your credit score is damaged for some reason, there are ways to improve it. We’ve mentioned earlier in this guide how 35 percent of your credit score is dependent on your payment history alone. When you take a personal loan and make the payments responsibly, your credit score goes up. With Best Rate Check, you can get pre-approved with multiple online lenders for free.

There are no credit checks from our end, no collateral requirements, and you won’t need to face heavy documentation processes. With just 2 details, you can be off to comparing the best loan offer with lower interest rates and flexible repayment terms. As you keep making timely payments, your credit score will improve.

This article does a great job explaining how payday loans work! For those looking for an alternative with more flexible repayment terms, online payday loans can be a great option. They allow borrowers to repay in scheduled payments rather than a lump sum, making budgeting easier. Always compare options to find the best fit for your financial needs!